The New York Times isn’t winning the news business. It’s escaping it

The Times found a business solution for journalism. It’s not selling news, and it’s not replicable.

For the media industry, it resembled the classic “good news, bad news.” The New York Times reported 1.35 million new subscribers, reaching a total of 12.8 million, on the exact same day The Washington Post revealed unprecedented layoffs: one-third of its staff, including 300 journalists.

Everyone, of course, read the Times’ 12.8 million figure as proof that journalism can still be profitable if you know what you’re doing. But is it? Is what The New York Times sells really journalism?

While the largest news orgs struggle to acquire another thousand, or even hundred, subscribers, The New York Times reports adding subscribers by the millions. How is that possible? Is it the logic of “the winner takes it all”? Many people in the industry and beyond tend to agree with this explanation, and it obscures the real question: what exactly those millions of Times subscriptions are.

Does the Times really sell news? Of course it does—an incredible volume of news. But is news what’s actually driving those 12.8 million subscriptions? Well, it’s complicated.

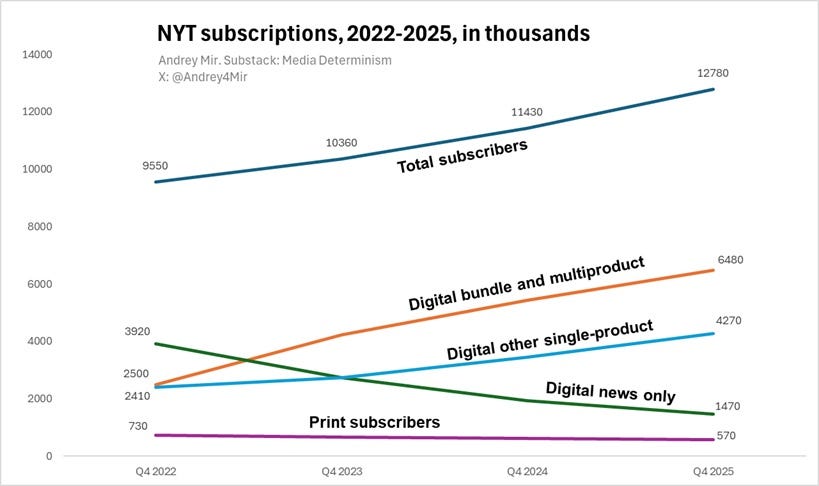

Look at the chart reflecting subscription dynamics for news, non-news products, and their bundles over the past four years.

It’s clear that core journalistic products—print newspapers and digital news-only subscriptions—have been in steady (print) and sharp (digital) decline. One might argue this is just price sensitivity: if news-only costs the same as a bundle that includes games, cooking, product reviews, and sports, readers will naturally choose the bundle. And the numbers confirm it—bundles are growing. But that also reveals the real driver: non-news products are what’s actually attracting subscribers. News is becoming the add-on, not the draw.

Financial data complement the picture of subscription dynamics. Unlike list prices, ARPU—average revenue per user—shows that, after promotional discounts wash out, NYT bundles generate roughly the same revenue per user as news-only subscriptions.

For Q3 2025, the ARPU numbers were:

Bundle and multiproduct: $12.84

News-only: $12.67

Other single product: $3.51

Total digital-only ARPU: $9.79

But bundles grow while news-only declines (see the first chart). What do these data say?

1. Digital “news-only” subscriptions remain a product for hardcore users who are willing to pay premium prices and have no interest in lifestyle content. This segment is substantial but shrinking.

2. Bundles, by contrast, cost the average user about the same as news alone but include entertainment and lifestyle content. This is where subscription growth—both in numbers and revenue—is coming from.

In other words, The New York Times has learned to sell news plus “something else” (see: “Journalism in search of a cute little monkey”). And that something else isn’t tote bags, wine clubs, events, or travel packages—the kinds of perks many publishers tried in 2012–2016. It’s lifestyle content that sits naturally alongside journalism: games, cooking, product reviews, sports.

Curiously, in the latest report (Q4 2025), the NYT announced it “will discontinue reporting digital-only subscribers and ARPU by the categories of bundle and multiproduct, news-only, and other single product.” In other words, the growth or decline of news and news-related subscriptions will no longer be publicly visible. The timing is telling: if a company is proud of its core business indicators, it promotes them, not “discontinues” reporting them.

It may even be fair to say that the overall subscription growth at the Times does not reflect but rather masks the actual state of the news business.

To push these speculations to their extremes:

1. The New York Times has grown its auxiliary content business to the degree that its news business is turning into an auxiliary business.

2. The New York Times is a content production platform that also happens to host a traditional newsroom and sell news.

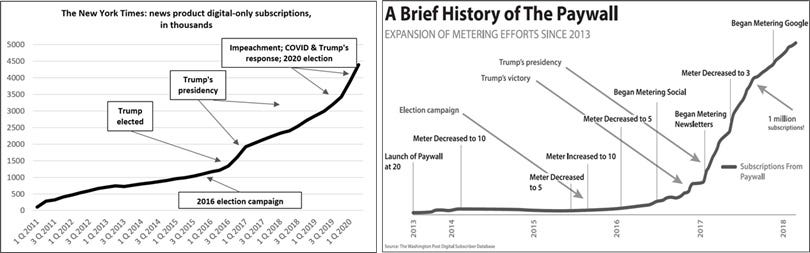

Make no mistake: both points reflect an incredible achievement and a unique business model the Times chose to build in response to the end of the Trump Bump—the surge in subscriptions driven by outrage-fueled coverage of Trump from 2016 to 2020. By 2020, it became clear that peak could not last. The Trump Bump may well have been the last gasp of news business in the 500-year history of journalism.

The Trump Bump—the surge in subscriptions at The New York Times and The Washington Post in 2016–2020. Charts from Postjournalism and the Death of Newspapers. The Media after Trump: Manufacturing Anger and Polarization.

The Times leadership recognized this and made a radical pivot. The model they pursued was no longer a news business but a platform business. When you build a distribution network with sufficient reach, you can sell anything through it. With really massive reach, you can even you can even sell “nothing,” like air or silence—the reach itself becomes value (see: “The Platform Paradox”).

So the question is: how much reach is needed to become a platform in the niche of mass media and adjacent content? The NYT invested heavily in growing its subscriber base, including acquiring The Athletic in 2022 (adding 1.2 million subscribers at once). In 2019, the Times set a goal of 10 million digital subscribers by 2025—they hit it in 2022. They’ve now set a new target: 15 million by 2027.

The New York Times keeps growing its subscription base, but that growth has slowed over the past three years. This suggests the platform may be approaching its natural limits. The recent decision to no longer report subscription statistics by categories may signal a shift in focus from extensive subscriber growth to more sophisticated product bundling. If the limits of growth are indeed being reached, then the intricate dance of bundling becomes even more important for extracting maximum value from each subscriber while retaining as many as possible.

Needless to say, this transformation required exceptional business and organizational talent to envision and execute. The New York Times:

seized the moment when other viable prospects for the news business had largely vanished,

leveraged its brand, arguably the strongest in the world, and

converted everything it had into a new business model.

This is what The New York Times business is today. It’s a content platform—a niche Amazon (sense the irony?). Actually, it’s exactly like Amazon in its early years, when it sold only books and used content products to build reach and then to sell whatever can be sold.

Where does journalism fit there? Somewhere inside—where it’s still fit to print.

However, another reading of this business model is also possible. At The New York Times, selling “something else”—sports, crosswords, recipes—subsidizes news production. This is remarkably similar to how advertising, comprising 80% of media revenue, subsidized journalism throughout the 20th century until the internet destroyed that model. Seen this way, The New York Times has found a new business model to maintain its news production at a level matching its brand. At least for now.

So it’s not “the winner takes it all”—not at all. It’s a new business model. And yet, how many media organizations can realistically build a subscriber base of 10+ million and transition from a news business to a platform business that subsidizes news? Except for the Times, likely none.

Update from February 22, 2026:

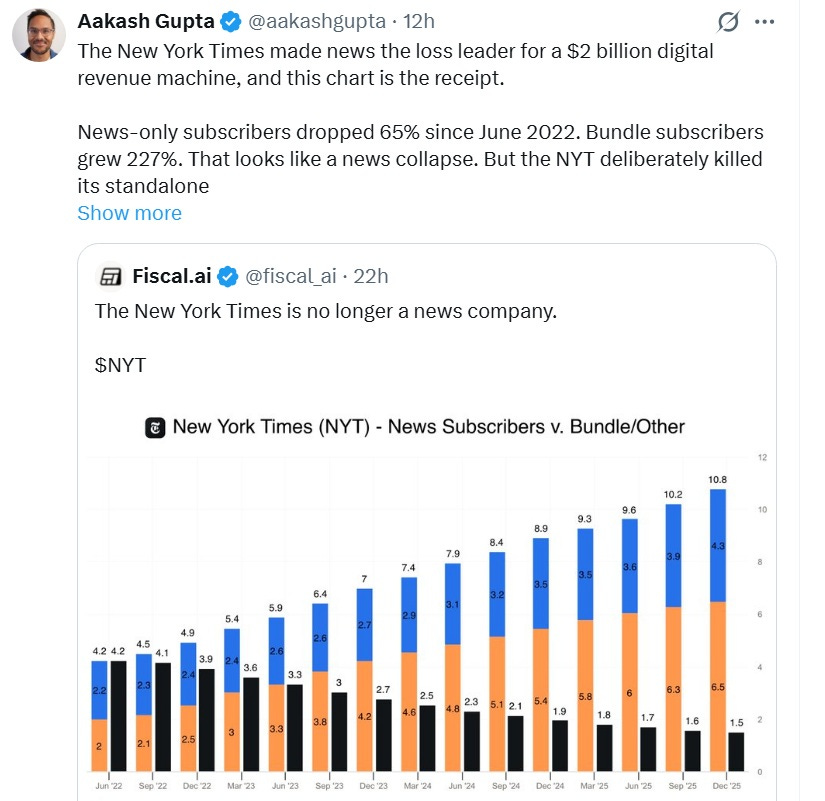

A slightly different angle by Aakash Gupta—Gupta comments on the chart that uses the same subscription data, but visually less compelling .

Gupta suggests that the NYT might deliberately suppress news-only subscriptions by charging high prices to foster readers’ (now rather users’) habit, or dependence on multiple products:

“That looks like a news collapse. But the NYT deliberately killed its standalone news product. They stopped marketing it. They made it nearly impossible to buy a news-only subscription on their website. They priced the full bundle (News + Games + Cooking + Athletic + Wirecutter) at $2/month introductory, cheaper than a standalone Games subscription....

This chart shows a news company that built an attention ecosystem where Wordle gets you in the door, Cooking keeps you at breakfast, The Athletic owns your commute, and by the time you think about canceling, you’d lose four products instead of one.

The NYT figured out that the way to fund journalism in 2026 is to make sure you can’t quit the crossword.”

Update from April 8, 2026.

In teh debate on why NYT does not have good engagement on X/Twitter, Joe Weisenthal posted an interesting chart:

It is also clear from the chart that the Trump bump (selling the Trump scare) exhausted its potential in 2021. The pandemic boost of 2020-21 was also the last gasp of the Trump bump.

The next, current surge in NYT valuation is a result of the new marketing strategy: building a platform large enough to sell bundles, with news becoming a secondary asset that is subsidized by the best-selling NYT product, entertainment bundles.

See other books by Andrey Mir:

The Viral Inquisitor and other essays on postjournalism and media ecology (2024)

Digital Future in the Rearview Mirror: Jaspers’ Axial Age and Logan’s Alphabet Effect (2024)

I understand today's news ‘flagships’ in their respective countries as working (once again) in the same light France’s Liberation functioned in the 70s: as a signaller of class. Intellectual class, open to anybody who subscribes to the prescribed political, economical and cultural positions (in name mostly, few New Yorkers want Mamdani to actually economically ‘succeed’ - 19 dead homeless is plenty proof of his ideological fervour).

The only difference is that in the 70s Liberation was literally physically carried under one's arm while strolling to the cafe for another bout of denouncing capitalism and imperialism - until dinner time. Since the NYT is now digital-heavy, signaling class happens through quoting the NYT. Next to dress, education, dating, being in shape, language, vehicle (EV) and of course one’s coiffure.

Verify this beyond what I say, but the rise of the bundle subscriptions may be caused in large part by the NYT putting in the additional offers sections that you could originally access through the normal subscription.

I for one know that I was once able to access the NYT cooking section with my subscription ; then one day I wasn't able anymore. I was pissed off, but I didn't use it enough to justify the subscription to the bundle. Same may go with the crosswords : I think you could get them through your normal subscription, originally. And in buying The Athletic, the NYT may have put all of its sport reporting in it, leaving sport enthusiasts with no other choice than to take an additional subscription.

This would mean that news still remain the main motive to subscribe, but that people are pushed to additional purchases in order to keep enjoying parts of the newspaper they were used to having.